5 Pros and Cons of Buying Your Next Home With a Reverse Mortgage Loan

Where you live in retirement influences your family life, hobbies, comfort, safety, cash flow, happiness and so much more.

Many people find that their housing needs change as they get older. For instance, your current home, though ideal for raising your family, may now be too big, outdated or difficult to maintain. You may desire a new home closer to your kids and grandkids. You may have your eyes on a home better suited for aging-in-place — such as an updated single-story, low-maintenance home with all the required amenities.

Although a change of scenery can benefit your well-being, moving later in life can be difficult. If you decide that moving is right for you, finding a home that aligns with your desired retirement lifestyle and funding the purchase in the best way for you and your retirement wallet is essential.

Historically, there have been two ways to purchase a new home: paying all cash or taking out a mortgage that requires monthly principal and interest payments. However, for homebuyers 62 and over, there’s a third option that offers the best of both worlds: a Home Equity Conversion Mortgage for Purchase (H4P) loan.

What Is an H4P Loan

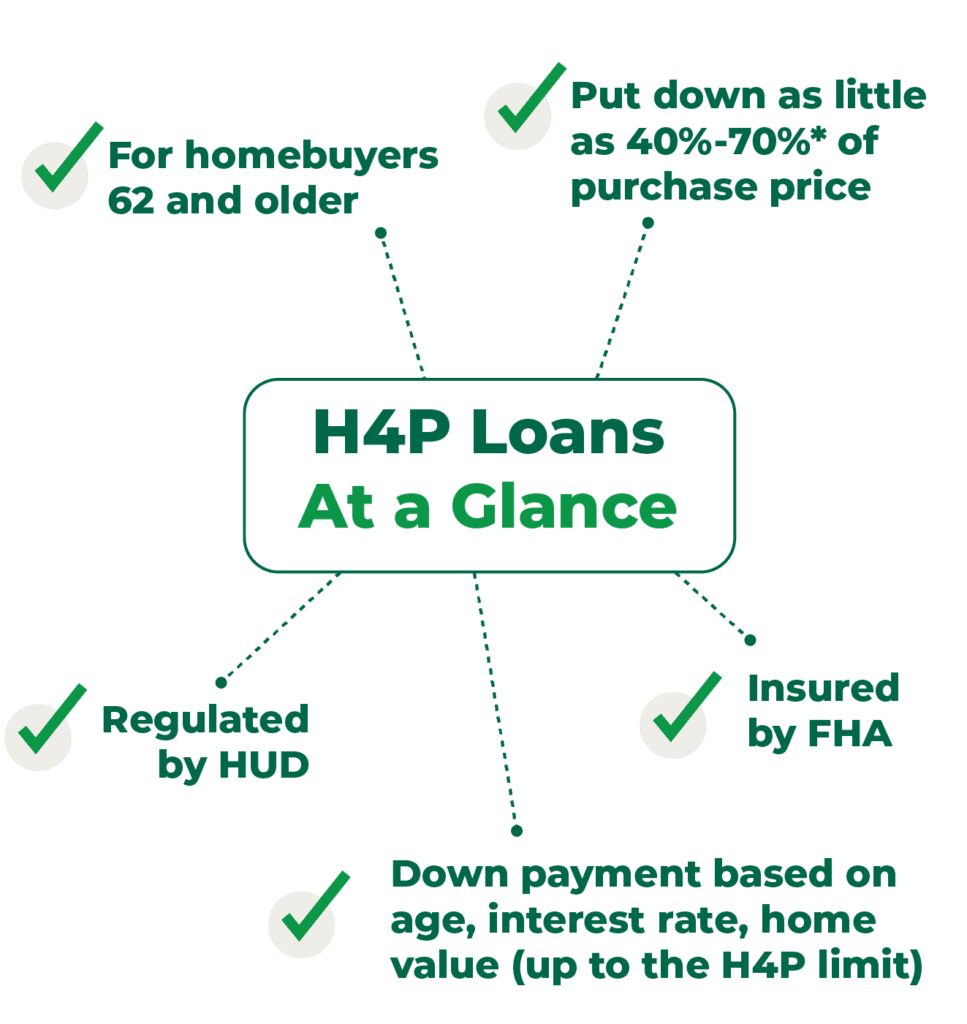

An H4P loan is a way for homebuyers 62 and older to buy a new primary residence in lieu of a traditional mortgage to finance part of the home’s cost. Introduced in 2008, the H4P program is only available through Federal Housing Administration (FHA)-approved lenders like Fairway Independent Mortgage Corporation.

Since its inception, the program has been regulated by the U.S. Department of Housing and Urban Development (HUD) and insured by the FHA. The H4P loan program can help those 62 and older more affordably downsize, rightsize or upsize into a new home and preserve retirement savings.

As with most traditional mortgage transactions, an H4P loan borrower must supply a down payment to supplement the H4P financing. As a homebuyer, you can purchase a new home by putting down as little as 40%-70%* of the purchase price from your funds, with the remainder funded by the H4P loan.

The down payment required is based on three factors: your age, the interest rate on the loan and the value of the home up to the H4P limit. You can get a ballpark idea of how much H4P loan proceeds you may be eligible for by using our online HECM for Purchase (H4P) calculator.

H4P Loan Pros

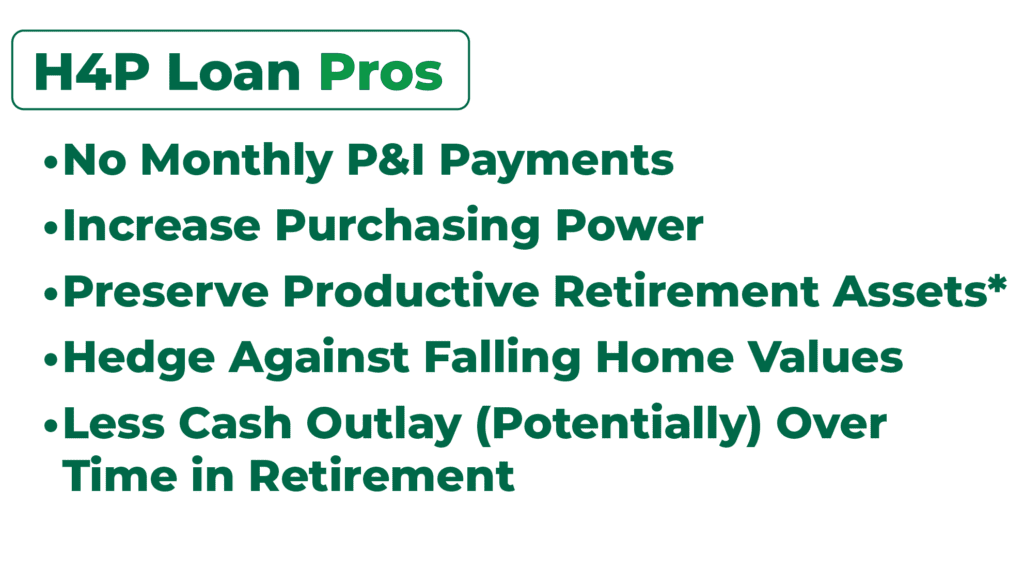

No Monthly Principal and Interest Mortgage Payments

You, as the borrower, can defer repayment of the loan balance so long as you live in the home, no matter how long that may be. You need to reside in the home as your primary residence, maintain it and pay critical property charges, like taxes and insurance.

Increase Purchasing Power

An H4P loan’s repayment flexibility can put your dream home within reach.

Preserve Productive Retirement Assets**

Cash that fully pays for a new home at closing or is committed monthly by way of required mortgage payments for the life of the loan will be tied up in that home, making it a very illiquid asset. There are opportunity costs to giving up all home sale proceeds and/or draining retirement savings to pay for your next home. An H4P can help you keep more of your retirement assets to use as you wish.

Hedge Against Falling Home Values**

As history has shown, the housing market can swing from a seller’s market to a buyer’s market and vice versa. No one knows for sure when the next housing market downturn will come.

Unlike a traditional mortgage, an H4P loan has a built-in feature that protects the homeowner against the risk of the home becoming upside down. The FHA insurance assures the borrowers will not be responsible for mortgage debt exceeding the home’s value.

In technical terms, an H4P loan is a non-recourse loan, which means neither the borrower nor their estate will owe more than the home’s value when the loan matures and the home is sold.*** Even if the property value drops or one or both borrowers live a very long time while deferring repayment, the homeowners can rest easy knowing they will not leave their heirs with a bill.

Less Cash Outlay (Potentially) Over Time in Retirement

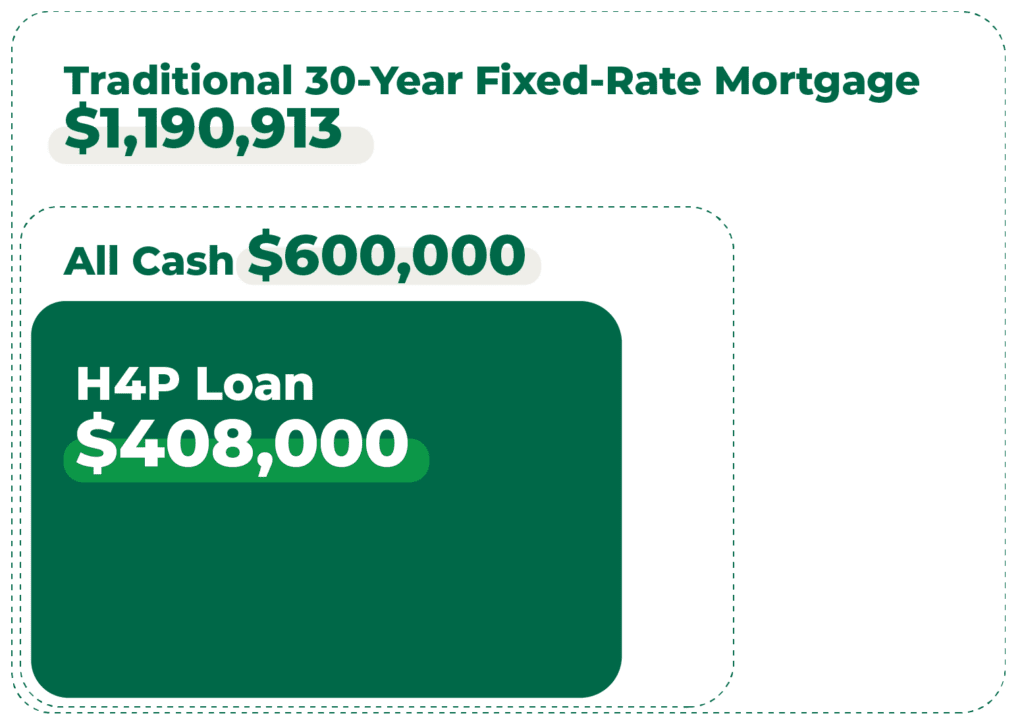

Here’s a hypothetical situation that compares the 30-year cash outlay based on home funding options for a 68-year-old to buy a $600,000 home.

NOTE: Story is for illustration purposes only. The persons depicted herein are fictional and any resemblance to actual persons is a coincidence.

Option 1: Pay All Cash

- 30-Year Cash Outlay (payment for the price of the home): $600,000

Option 2: Take Out a Traditional 30-Year Fixed-Rate Mortgage

- Down Payment (20%): $120,000

- Estimated Closing Costs: $15,000

- Loan Amount: $480,000

- Interest Rate: 7.22%

- APR: 7.433%

- Term: 30 years

- Monthly Mortgage Payment (principal and interest): $3,725

- 30-Year Cash Outlay (upfront payment + total required monthly principal and interest mortgage payments): $1,190,913

Option 3: Using an H4P Loan

- Down Payment (65%): $390,000*

- Loan Amount: $210,000* ***

- Estimated Closing Costs: $18,000 Initial Rate: 7.125%

- Total Monthly Mortgage Payment (principal and interest): Optional — $0 required*****

- 30-Year Cash Outlay (upfront payment): $408,000

H4P Loan Cons

Unpaid Loan Balance Accrues Compounding Interest (Negative Amortization)

An unpaid outstanding HECM loan balance accrues both interest and annual Mortgage Insurance Premium (MIP), causing the unpaid balance to rise over time. You can make voluntary prepayments toward the loan balance at any time. Generally, the loan becomes due and payable after the last surviving borrower passes away. To keep the home, heirs would have to pay off the loan.

Note: Both initial MIP and annual MIP end up in the Mutual Mortgage Insurance Fund. The FHA uses this fund to pay claims when the home sells for less than the loan balance. Again, this is the non-recourse guarantee that the borrower and their heirs are never stuck with a bill when the loan becomes due and payable.

Borrower Must Meet Loan Obligations To Continue Deferring Loan Balance Repayment

The loan can become due and payable if obligations are not met, such as failing to pay property-related taxes and insurance. That’s why a financial assessment is necessary—the loan must be a sustainable solution and the prospective borrower must show a willingness and the capacity to pay the ongoing property charges.

Lien Against the Home

While the borrower remains on title and owns the home, there is a lien against the home until the mortgage is satisfied.

Required Initial Monetary Investment Higher Than a Traditional Mortgage (Typically)

While a traditional mortgage commonly requires putting down about 20% of the purchase price, plus closing costs, an H4P loan requires placing down about half of the purchase, plus closing costs and other fees.

The initial Mortgage Insurance Premium is the most considerable upfront cost. The cost is the lesser of:

- 2% of the home value, or

- 2% of the HECM limit (currently $1,249,125)

For example, if the home value is $423,000, after calculating 2% of $423,000, your initial MIP cost would be $8,460. Other upfront costs may include an origination fee and third-party closing costs.

Home Must Be the Borrower’s Primary Residence

The home must be purchased for use as the borrower’s principal residence. The H4P program has an annual certification process in which the borrower must confirm that the home is still their primary residence.

Let’s Start a Conversation!

If you’re interested in learning more about H4P loans and if one might be right for you or a loved one, Fairway Independent Mortgage Corporation can help. Connect with us today.

Copyright©2023 Fairway Independent Mortgage Corporation (“Fairway”) NMLS#2289. 4750 S. Biltmore Lane, Madison, WI 53718, 1-866-912-4800. All rights reserved. Fairway is not affiliated with any government agencies. These materials are not from HUD or FHA and were not approved by HUD or a government agency. Reverse mortgage borrowers are required to obtain an eligibility certificate by receiving counseling sessions with a HUD-approved agency. The youngest borrower must be at least 62 years old. Monthly reverse mortgage advances may affect eligibility for some other programs. This is not an offer to enter into an agreement. Not all customers will qualify. Information, rates and programs are subject to change without notice. All products are subject to credit and property approval. Other restrictions and limitations may apply. Equal Housing Opportunity.

The required down payment on your new home is determined on a number of factors, including your age (or eligible non-borrowing spouse’s age, if applicable); current interest rates; and the lesser of the home’s appraised value or purchase price.** This advertisement does not constitute tax or financial advice. Please consult a tax and/or financial advisor regarding your specific situation. *** There are some circumstances that will cause the loan to mature and the balance to become due and payable. Borrower is still responsible for paying property taxes and insurance and maintaining the home. Credit subject to age, property and some limited debt qualifications. Program rates, fees, terms and conditions are not available in all states and subject to change. ****Negative amortization could cause the total amount due at the end of the loan to increase if optional***** reverse mortgage payments are not made. The example is used for illustration purposes only. The information is used for illustration purposes only. The information is provided as a guideline; the actual reverse mortgage available funds are based on current interest rates, current charges associated with the loan, borrower date of birth, the property sales price, and standard closing cost. *****Borrower must remain current on property taxes, homeowner’s insurance (and homeowner association dues, if applicable), and home must be maintained.