Debunking Reverse Mortgage Myths: Get the Facts

Debunking common myths around reverse mortgages.

When reverse mortgage loans were first introduced in the early 1960s, they did not have any government programs backing it. Today, most, but not all, reverse mortgages are insured through the Federal Housing Administration (FHA)’s Home Equity Conversion Mortgage (HECM) Program.

In recent years, the FHA and U.S. Department of Housing and Urban Development (HUD) have made many amendments to the HECM program to improve consumer protections. This blog talks about HECM loans only.

If you ask people what they think about reverse mortgages, you are sure to get some strong opinions. Unfortunately, many people form those opinions based on misconceptions about the way reverse mortgages work.

At Fairway, we are committed to educating you on the facts about reverse mortgage so you can make an informed decision about one of your most valuable assets: your home. Some of the most common myths around reverse mortgages that we hear are compiled below.

And if you’re curious what you may qualify for, you can use our free reverse mortgage calculator!

Reverse mortgage myth #1: I could lose my house and be forced to move.

FACT: As long as all loan terms are met, you cannot be forced to sell the home and move. Terms include

living in the house as your primary residence, maintaining the home, and paying home expenses such as

taxes and insurance. Some circumstances will cause the loan to mature and the balance to become due and payable. Credit is subject to age, property and some limited debt qualifications. Program rates, fees, terms, and conditions are not available in all states and subject to change.

Reverse mortgage myth #2: Your home will be taken away when you pass away, and the family loses the right to the property.

FACT: When you permanently move out of the home, whether you sell it or pass away, neither you, your estate nor your heirs are responsible for paying the deficit if the balance owed on your reverse mortgage exceeds the home value. However, should your heirs want to keep your home, they may purchase it for 95% of the current appraised value.*

Reverse mortgage myth #3: Your house must be debt-free to qualify for a reverse mortgage.

FACT: The amount of money you qualify for a reverse mortgage varies based on the down payment you will need to bring to closing (ranges from 50 – 74%), which will be determined based on your age, or age of nonborrowing spouse, if applicable, current interest rates and the sales price (or appraised value, whichever is less) of the home you are buying. You must live in the house as your primary residence (live there 6+ months per year). Some income, property, and credit qualifications apply to ensure you can pay taxes and insurance and maintain the home.

Reverse mortgage myth #4: The safest thing is a house “free and clear.”

FACT: In the event of an extended nursing home stay or a lawsuit, all your home equity can be lost that you spent your whole life to create. A reverse mortgage loan can unlock that equity and allow you to manage it for the benefit of your family properly. Talk to your financial advisor about how a reverse mortgage can help you do this, including helping you pay for longer-term expenses such as medical and nursing home expenses.

Reverse mortgage myth #5: I will be giving up the deed to my own home, and I will not own it anymore.

FACT: The deed is still in your name so you can move whenever you want. Most reverse mortgages are federally insured through the FHA. As long as you pay your property taxes, homeowner’s insurance and maintain your home you cannot be foreclosed on. We must honor this commitment for life or as long as you live in your home. However, you are allowed to change your mind and sell the house whenever you want if you wish to move to warmer climates, a right size home, or closer to your children whatever your choice may be. Only you will make the decision, not the lender or the government.

Reverse mortgage myth #6: A Reverse mortgage doesn’t offer anything different from other loans but costs more.

FACT: There have been changes in FHA’s reverse mortgage program in recent years that reduced a borrower’s costs. While any reverse mortgage is still more expensive than a traditional mortgage, they may provide you with more options than a conventional mortgage, such as no mortgage payments, (borrower is still responsible for paying taxes and insurance and maintaining the home), and an increasing line of credit option on unused funds.

Reverse mortgage myth #7: My children could get stuck with a big mortgage if I live too long.

FACT: Since this is a non-recourse loan, even if your home value decreases, you and your children can never be liable for any amount over the value of the home* because the loan is guaranteed by the Federal Housing Administration (FHA) Mortgage Insurance Fund (FHA/HUD).

Reverse mortgage myth #8: A reverse mortgage is a government benefit.

FACT: A reverse mortgage is a non-recourse loan because of the guarantees authorized by the government. Mortgage Insurance Premiums (MIP) paid by the borrowers fund this FHA program. The taxpayers do not support the program; it is made possible by FHA, who monitors lenders ensuring that consumers are treated fairly and equitably.

Note: While Fairway as the lender does loan the money for the reverse mortgage loan, it is not affiliated in any way with any government agencies. These materials are not from HUD or FHA and were not approved by HUD or a government agency.

Reverse mortgage myth #9: A reverse mortgage loan should only be considered as a loan of last resort.

FACT: Many folks think a reverse mortgage can only be used when all other accounts and options are exhausted. While it can be a great way to add cash flow for a borrower 62 and better that has fallen on hard times (including, potentially foreclosure situations**), a reverse mortgage is also an appealing option when used earlier in retirement to help avoid future problems by keeping the home safe with the retiree “aging in place.”

In fact, many people use a reverse mortgage loan as a part of a strategic retirement plan.

Reverse mortgage myth #10: To qualify for a reverse mortgage, both spouses need to be 62+.

FACT: Only one borrower(s) must be 62 or better—except in Texas, where both spouses need to be at least 62. To be eligible for a reverse mortgage, The home must be a primary residence (live there 6+ months per year) and either have significant equity or be owned outright to qualify. The property must be a single-family home, 2-to 4-unit dwelling or FHA-approved condo. Borrower(s) much receive a reverse mortgage counseling certification from a HUD-approved counseling agency.

Reverse mortgage myth #11: If you don’t qualify for traditional financing, you will not be eligible for a reverse mortgage loan.

FACT: A reverse mortgage loan does not have any income qualifications such as needing a certain Debt To Income (DTI) ratio or credit score requirements. In 2015, FHA added financial assessment requirements to determine if a Life Expectancy Set Aside (LESA) will be necessary or not. The residual income requirement must be met with regular income or compensating factors to proceed with the loan. Just because a LESA may be required, it will not prevent you from getting a reverse mortgage loan if you have enough equity or cash reserves to bring to closing.

Reverse mortgage myth #12: You have limited options of how you can receive and use the proceeds from a reverse mortgage loan.

FACT: Unlike a traditional mortgage, which is usually a lump sum, there are a variety of ways you can receive the proceeds from a reverse mortgage. You can receive funds via a single, lump sum disbursement; a line of credit; or fixed monthly advances (tenure or term). The funds can be used for anything that you wish.

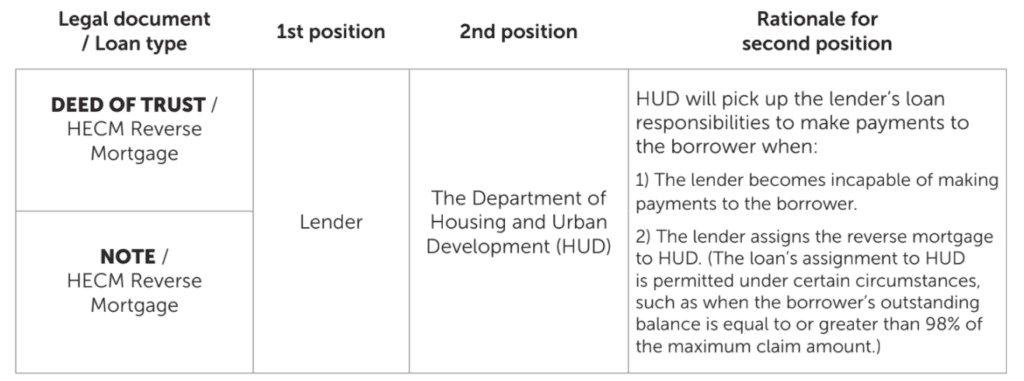

Reverse mortgage myth #13: The deeds and notes are unclear

When signing reverse mortgage loan documents, borrowers are sometimes confused when the notary gives them TWO Deeds of Trust and TWO Notes to sign. So, let’s clear up why there are two of each.

With a reverse mortgage, you get an advance on part of your home equity and you are not required to make a monthly mortgage payment. You just need to pay taxes, insurance, and maintain the home. While the lender (e.g., Fairway) is responsible to make payments to you as the borrower, there may come a time when the Department of Housing and Urban Development (HUD) would assume that responsibility.

So, the second Deed of Trust and second Note secure any payment which might be made by HUD to you as the borrower—those documents are required to be signed by you in order for HUD to insure the loan.

15 fast facts about reverse mortgages

- There are over 9 trillion dollars of untapped home equity in Baby Boomers’ homes***.

- Reverse Mortgages have an 83% satisfaction rating for borrowers who have a reverse mortgage loan according to a study done by Ohio State University****.

- With a reverse mortgage, you have the option to repay as much or as little of the loan balance each month as you would like, or you can make no monthly mortgages payments at all. Of course, you must still maintain the home and pay homeowners insurance and property taxes.

- The FHA-insured Home Equity Conversion Mortgage (HECM) was signed into law on February 5, 1988, as part of the Housing and Community Development Act of 1987.

- A Reverse Mortgage Line of Credit has a growth feature—giving the borrower access to even more funds in retirement (applies to unused funds).

- The age to qualify for a reverse mortgage loan is 62 or older.

- With a reverse mortgage, as long as all loan terms continue to be met, the non-borrowing spouse can still live in the home should the borrower predecease them. Terms include living in the house as your primary residence, maintaining the home, and paying home expenses such as taxes and insurance.

- Mortgage insurance is built into every reverse mortgage loan.

- Borrowers can escrow the taxes and insurance over the life of the reverse mortgage through a Life Expectancy Set-Aside (LESA).

- Qualifying for a reverse mortgage loan does not include a specific credit score. (However, minimal credit, income, and property qualifications do apply.)

- Your heirs are still entitled to the remaining equity balance, if any, after the loan has been paid off. (This does not constitute legal advice. Please consult an attorney for your specific situation.)

- All borrowers must get HUD-approved counseling prior to getting a reverse mortgage loan.

- The maximum claim amount on a HECM reverse mortgage loan is now $1,209,750, as of January 1, 2023.

- Accessing a portion of your home equity with a reverse mortgage loan early on could potentially allow all of your investments to last longer.**

- The proceeds from a reverse mortgage loan can be used to help divide assets in a divorce.**

Want to learn more about reverse mortgage options for you?

*There are some circumstances that will cause the loan to mature and the balance to become due and payable. The borrower is still responsible for paying property taxes and insurance and maintaining the home. Credit subject to age, property and some limited debt qualifications. Program rates, fees, terms, and conditions are not available in all states and subject to change.

** This advertisement does not constitute legal or financial advice. Please consult a legal or financial advisor for your specific situation.

***https://www.nrmlaonline.org/about/press-releases/senior-housing-wealth-exceeds-record-9-2trillion/rmmi-q12021

****Source: https://reversemortgagedaily.com/2016/03/13/study-reverse-mortgage-borrowers-report-high-satisfaction-levels/