Why Today’s Interest Rates Shouldn’t Stop You From Improving Your Future

Making major decisions involving one’s home can be stressful, so it’s only natural to want to wait for the perfect time to do so. But in real estate, as in life, perfect opportunities rarely come along, and often, we only see those opportunities for what they were in hindsight.

A common concern for retirees wanting to increase their cash flow with a reverse mortgage loan is today’s interest rates. The average home mortgage interest rate topped 7% in August 2023, making it the highest in over 20 years. While it most certainly is true that interest rates affect the costs of reverse mortgage loans, that is only one element of the overall value a reverse mortgage can offer.

Home Values and Reverse Mortgage Loans

Although today’s mortgage interest rates are high, average home values are a bright silver lining for reverse mortgage loan borrowers, many of whom bought their houses quite some time ago. For example, from 2000 to 2020, the median national home price rose by 99%. From 2020 to Q2 2023 alone, home values rose 26%.

How Are Home Values, Interest Rates and Reverse Mortgage Loans Related?

While there are several types of reverse mortgages, the Federal Housing Administration (FHA)-insured Home Equity Conversion Mortgage (HECM) accounts for the large majority of U.S. reverse mortgages.

A HECM enables homeowners 62 and over to convert a portion of their home equity into tax-free cash.* The higher the appraised value of a home, the greater the potential proceeds from a reverse mortgage loan. Think of it like a portion of a pie. If it’s divided evenly into slices, you get more for your money if the pie grows in size.

The amount of money one can borrow from a HECM is called the principal limit. Your initial principal limit, determined during the loan approval process, is a calculation based on three factors:

- The age of the youngest borrower (or eligible non-borrowing spouse, if applicable)

- The expected rate on the loan

- The lesser of the home value or the HECM limit (currently $1,249,125)

The Dept. of Housing and Urban Development (HUD) provides HECM lenders with a HECM Principal Limit Factor (PLF) calculation table, which determines HECM proceeds based on the above factors.

Generally speaking, a younger borrower, a higher expected rate and a lower-value home will have a lower principal limit than an older borrower, a lower expected rate and a higher-value home.

Increasing your age is the only factor in the equation you can control. What both the expected rate and the home value will be months or years down the road are two big unknowns driven by external market factors. If you decide to wait and expected rates rise and/or home values fall, you might not end up with a larger principal limit.

Curious what you may qualify? Use our free reverse mortgage calculator to find out!

Why You Shouldn’t Count on Home Values Staying This High for Long

Interest rates and home values typically have an inverse relationship: the higher the interest rates, the lower the prices of homes. The current home value highs are anomalous in many regards and result primarily from a lack of new houses for sale.

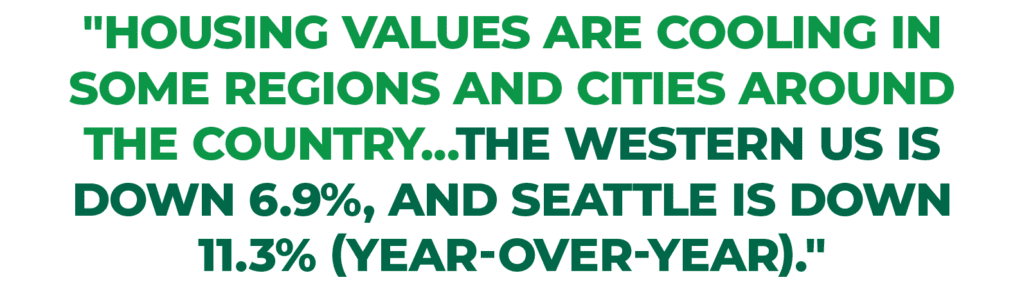

Housing values are cooling in some regions and cities around the country. For example, the Western US is down 6.9%, and Seattle is down 11.3% (year-over-year).

Although there are many different opinions on the direction of the housing market over the next few years, many experts predict that price gains are near their peak for 2023. That means right now may be the best time to act regarding home value and equity if you’re considering a reverse mortgage loan.

Don’t Forget About Inflation and Market Volatility

Despite interest rate hikes meant to stabilize prices, inflation rose 3.2% from July 2022 to July 2023. While many economists hope the U.S. has avoided an imminent recession, markets remain highly volatile. An economic slowdown in China, fears over a conflict in Taiwan and the war in Ukraine are just some of the unpredictable factors that have devalued stocks and bonds for millions of people.

Inflation and market volatility are especially dangerous for retirees on a fixed income. Prices for essentials and luxuries continue to rise while portfolio values and income from dividends, interest and capital gains are far less reliable.

Reverse Mortgage Loans as a Buffer Strategy*

The result for many seniors is that their money doesn’t go as far as it used to, and there’s far less of it to go around. This can cause many to sell off assets at a loss, potentially jeopardizing a retiree’s financial stability over time. If unexpected expenses crop up during a downturn, many seniors can find themselves in a very stressful financial reality.

In response, many financial advisors recommend using a reverse mortgage loan as a buffer strategy. Homeowners can use their loan proceeds to cover their expenses during market downturns or unexpected expenses, in general, to protect their retirement assets in down markets.*

Check out this quick testimonial video from Tod, a retired financial advisor and Fairway reverse mortgage loan customer. He uses his reverse mortgage as a buffer strategy and has been thrilled with the results!

Waiting Sacrifices Compounding Line of Credit Growth

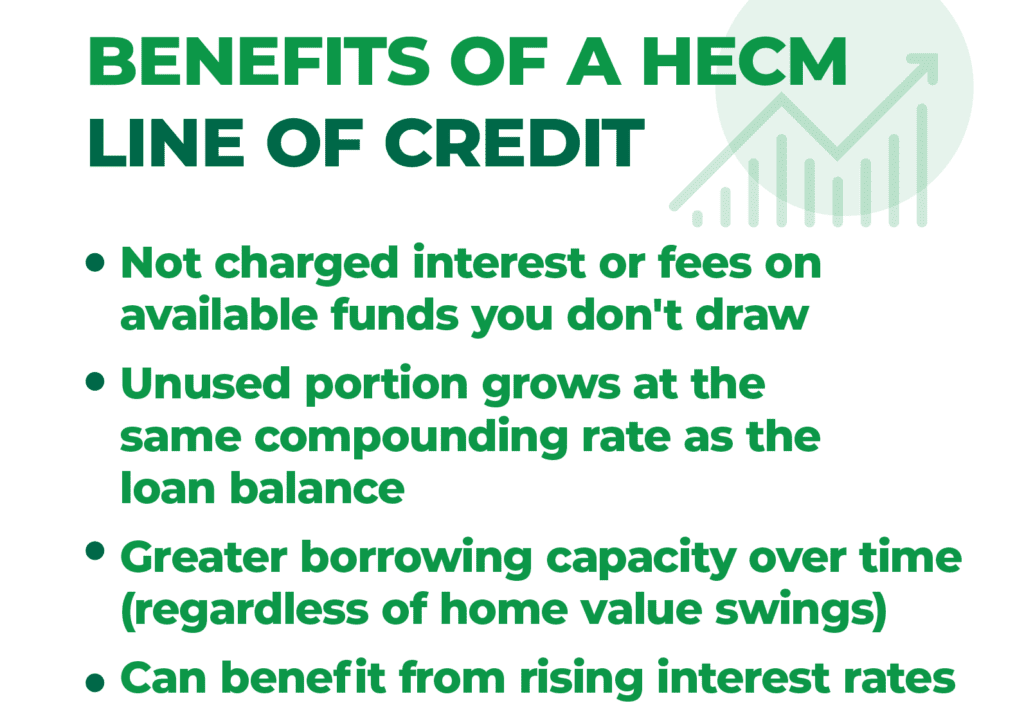

If you take out a reverse mortgage line of credit, you’re not required to borrow any of the available funds — ever — and you’re not charged interest or fees on the available funds you don’t draw.

Better yet, the unused portion of the line of credit grows over time, meaning you’ll have greater borrowing capacity as the months and years pass, regardless of swings in your home’s value. The unused portion of the line of credit grows at the same compounding rate (the interest rate plus 0.50%) as the loan balance.

Any voluntary prepayments you make toward your line of credit loan balance increase your borrowing capacity dollar-for-dollar. You can borrow the paid-down amount again or leave it alone in the line of credit and watch it grow. When you establish a line of credit early and defer or limit its use, a rising interest rate environment can work in your favor, as your borrowing capacity will increase faster.

The sooner-than-later strategy with the HECM line of credit can give you greater financial flexibility and security over a lengthy retirement.

Eliminating Monthly Mortgage Payments

One of the primary benefits of a reverse mortgage loan is that borrowers are not required to make monthly mortgage payments going forward. Instead, they simply have to take care of property charges, like taxes, insurance and home upkeep. Those who own their homes outright have much greater potential loan proceeds.

If you’re making monthly mortgage payments in retirement, eliminating them is an excellent reason to act now on a reverse mortgage loan. That guaranteed outflow of money is challenging for most on a fixed income, especially in times of inflation and market volatility. In fact, for many homeowners, a monthly mortgage payment is the last roadblock to retirement! That alone is reason enough to pursue a reverse mortgage sooner rather than later.*

Whether you use your reverse mortgage loan proceeds to refinance an existing mortgage or for other purposes like home improvements, it’s great peace of mind to know your monthly mortgage payment will always be $0 – so long as you live in the home, maintain it and pay critical property charges, like taxes and insurance.

Find Out if Now Is the Right Time for You

It’s easy to miss out on a great opportunity if you’re only willing to act when everything seems perfect. Many senior homeowners may be focused on less-than-ideal interest rates while missing out on the chance to significantly improve their financial well-being now and for years to come.

Only by understanding the dynamics between a home’s value, interest rates and the unique advantages of reverse mortgage loans can a homeowner make a truly informed decision. If you’re interested in finding out if now is the right time for a reverse mortgage loan, our specialists are happy to help you find the answer.

Find Out More About Our Loans, Like How Much You May Qualify For

Please fill out the form below and we’ll be in touch!

*This article does not constitute tax/financial advice from Fairway. Please consult a tax/financial advisor regarding your specific situation.

Copyright©2023 Fairway Independent Mortgage Corporation (“Fairway”) NMLS#2289. 4750 S. Biltmore Lane, Madison, WI 53718, 1-866-912-4800. All rights reserved. Fairway is not affiliated with any government agencies. These materials are not from HUD or FHA and were not approved by HUD or a government agency. Reverse mortgage borrowers are required to obtain an eligibility certificate by receiving counseling sessions with a HUD-approved agency. The youngest borrower must be at least 62 years old. Monthly reverse mortgage advances may affect eligibility for some other programs. This is not an offer to enter into an agreement. Not all customers will qualify. Information, rates and programs are subject to change without notice. All products are subject to credit and property approval. Other restrictions and limitations may apply. Equal Housing Opportunity.