Debunking the Top 15 Reverse Mortgage Loan Myths

A reverse mortgage is a unique home loan that allows older homeowners to access their home equity while deferring repayment until they move, sell or pass away. Although monthly mortgage payments aren’t required, borrowers must cover essential property charges like taxes and insurance.

Despite the many benefits, misconceptions stemming from outdated views and a lack of understanding about today’s reverse mortgage loans often deter older homeowners from considering this product.

Most reverse mortgages today are insured by the Federal Housing Administration (FHA) through the Home Equity Conversion Mortgage (HECM) program. In this article, we’ll debunk the most persistent HECM reverse mortgage myths, giving you the knowledge to make a confident decision.

This article covers:

- Myth #1: It’s only useful as a loan of last resort.

- Myth #2: The bank gets your home.

- Myth #3: You can’t leave your home to your heirs.

- Myth #4: Your heirs will get stuck with a huge bill.

- Myth #5: You must own your home free and clear to qualify.

- Myth #6: You can’t keep your home in a trust.

- Myth #7: It’s a taxpayer-funded bailout.

- Myth #8: You have limited options for spending the loan proceeds.

- Myth #9: It will disrupt your Social Security and Medicare benefits.

- Myth #10: You can’t use a reverse mortgage loan to buy a home.

- Myth #11: Both spouses must be at least 62 years old.

- Myth #12: You might outlive a reverse mortgage.

- Myth #13: Reverse mortgages are never worth the costs.

- Myth #14: Getting a fixed-rate reverse mortgage is always best.

- Myth #15: You won’t ever be able to sell and move.

Myth #1: It’s only useful as a loan of last resort.

This versatile home loan can benefit a wide range of older homeowners—from the affluent wanting to diversify home equity to grandparents wishing to live closer to family.

Now more than ever, financial advisors and consumers recognize reverse mortgages as valuable for financial planning.* They offer emergency funds, lifestyle enhancements and long-term financial opportunities with a growing line of credit (growth applies to unused funds).

Myth #2: The bank gets your home.

Contrary to popular belief, you retain home ownership with a reverse mortgage. As long as you cover essential property charges, like taxes and insurance, and live in and maintain your home, you can’t be foreclosed on. The reverse mortgage just places a lien on your home, much like a traditional mortgage or home equity loan.

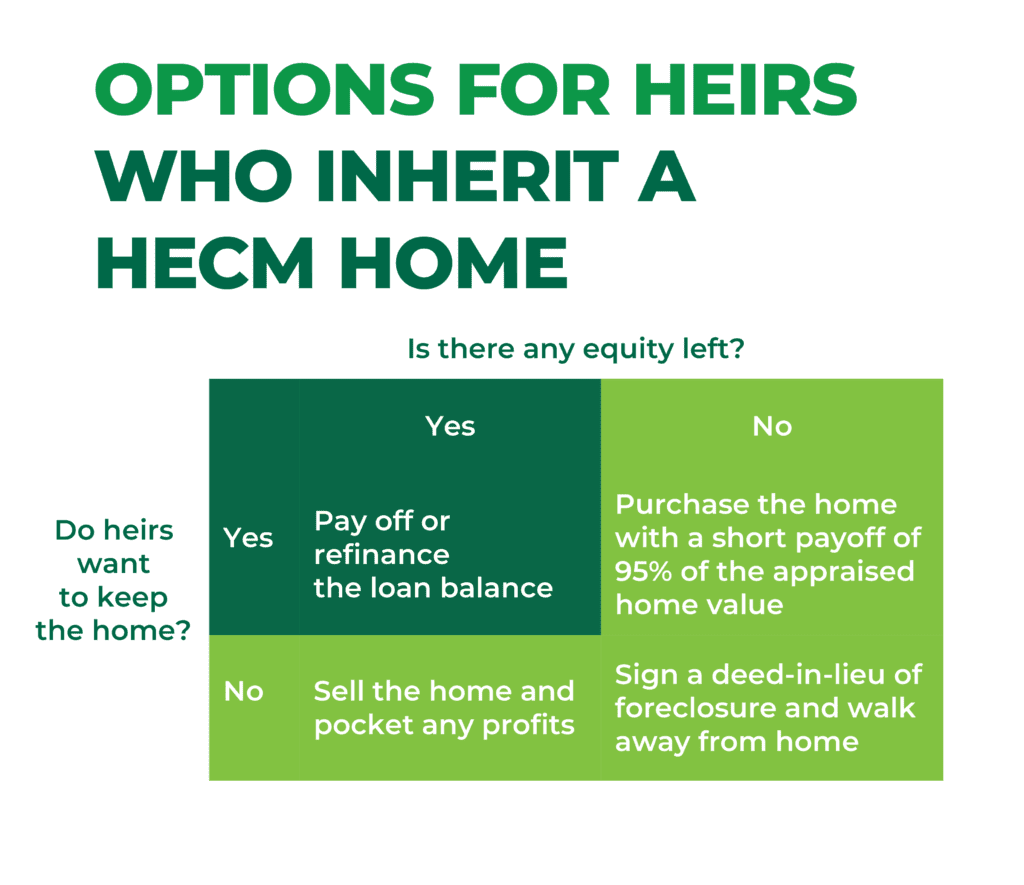

Myth #3: You can’t leave your home to your heirs.

Your heirs can inherit your home. After the last surviving borrower passes away, the reverse mortgage becomes due, and your heirs have options:

If they want to keep the home, they can pay off or refinance the lesser of the outstanding loan balance or 95% of the home’s appraised value.

If they don’t want to keep the home, they can sell the property and keep any profit, or, if there’s no financial benefit, sign a deed-in-lieu of foreclosure and walk away.

Myth #4: Your heirs will get stuck with a huge bill.

Rest easy knowing your heirs won’t be left with a big bill. Thanks to the non-recourse feature, you and your heirs are protected, never owing more than the home’s value when the loan becomes due and the home is sold. The debt is secured by the home itself, ensuring neither you nor your heirs can be held personally liable for any excess debt.** For HECMs, this non-recourse guarantee is backed by the FHA.

Myth #5: You must own your home free and clear to qualify.

There’s no need to have your mortgage paid off before closing! Any mortgage debt on the home must be paid off at closing, and you can use reverse mortgage proceeds to do just that. Essentially, you’re swapping a monthly payment-required mortgage for a payment-optional reverse mortgage. You’ll still need to cover essential property charges like taxes and insurance.

Myth #6: You can’t keep your home in a trust.

You may be able to keep the title to your home in a trust if you get a reverse mortgage loan. Let your loan officer know early so the lender and title company can review your trust documents. Most trusts meet the requirements, but it’s wise to confirm early to avoid any surprises.

Myth #7: It’s a taxpayer-funded bailout.

Taxpayer dollars don’t fund reverse mortgages. The FHA insures HECM reverse mortgage loans, ensuring borrowers and heirs never owe more than the home’s value at sale.** This protection is funded by Mortgage Insurance Premiums (MIPs) collected from borrowers, not taxpayers. These premiums go into the FHA’s Mutual Mortgage Insurance Fund, which covers any shortfall between the sale price and the loan balance.

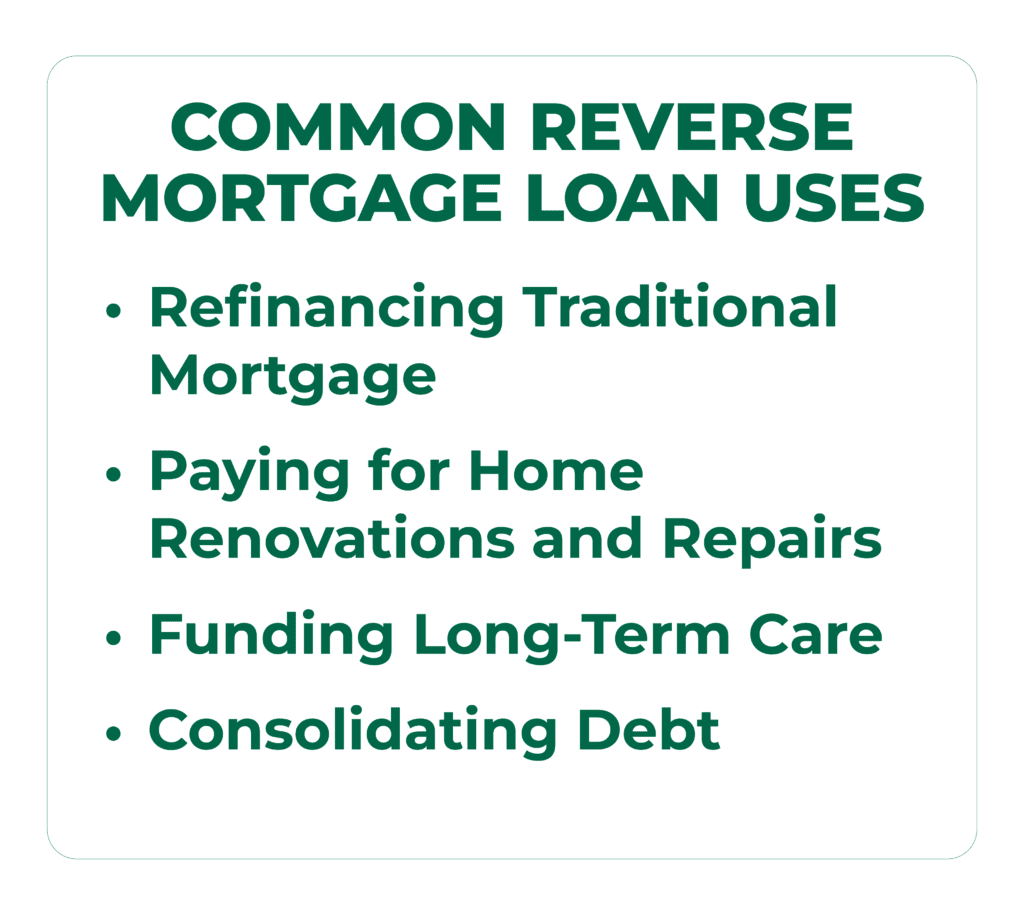

Myth #8: You have limited options for spending the loan proceeds.

Reverse mortgage loan proceeds can be used for just about any purpose. Common uses include refinancing a traditional mortgage, paying for home renovations and repairs, funding long-term care and consolidating debt. Reverse mortgage funds are generally not considered income and, therefore, are not usually taxed as such.*

Myth #9: It will disrupt your Social Security and Medicare benefits.

Distributions from a reverse mortgage typically don’t affect Social Security or Medicare benefits. However, if you receive Medicaid, consult a benefits administrator. Medicaid rules vary by state, and placing reverse mortgage funds in your bank account could impact your eligibility due to asset thresholds.

Myth #10: You can’t use a reverse mortgage to buy a home.

With the HECM for Purchase (H4P) program, you can buy a new home. By bringing the required funds to closing as a down payment,*** you generate the necessary equity. After closing, the loan functions just like a reverse mortgage on a home you’ve owned for years.

Myth #11: Both spouses must be at least 62 years old.

Only one spouse must be 62 or older to qualify—except in Texas, where both must meet the age requirement.

Myth #12: You might outlive a reverse mortgage.

While the mortgage note includes a maturity date of age 150, if you reach that incredible milestone, the U.S. Department of Housing and Urban Development (HUD) allows the security instrument to be re-recorded, ensuring continued coverage.

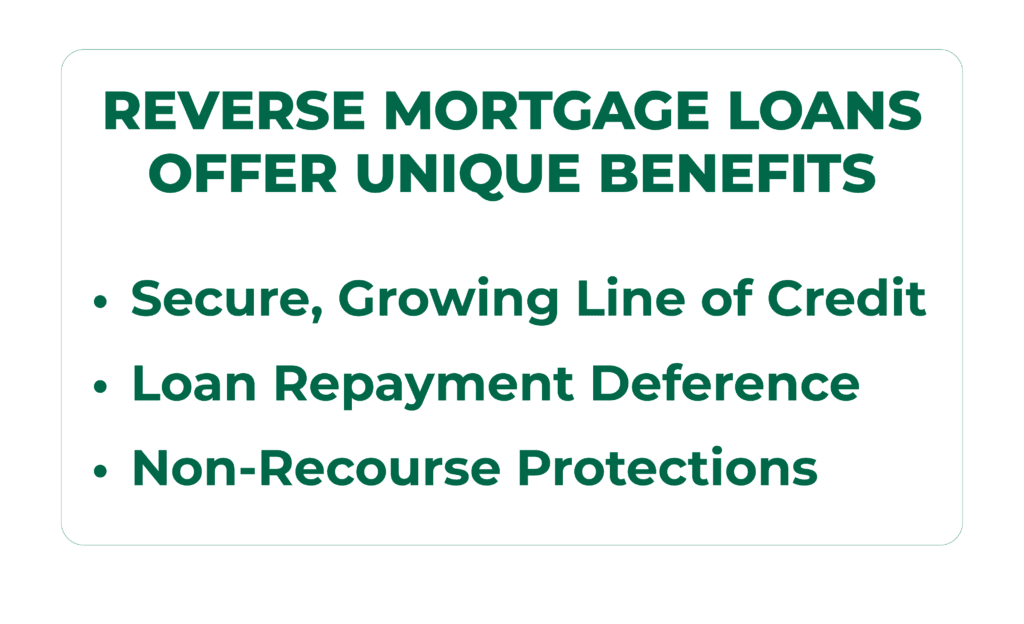

Myth #13: Reverse mortgages are never worth the costs.

Reverse mortgages are generally pricier than traditional mortgages, but they offer unique benefits tailored for older homeowners. The opportunity costs of not getting a reverse mortgage—such as missing out on a growing line of credit (applies to unused funds), deferring loan repayment and having a non-recourse loan—can outweigh the upfront and ongoing expenses.

Myth #14: Getting a fixed-rate reverse mortgage is always best.

A reverse mortgage can be fixed- or adjustable-rate, each with different payout options. Fixed-rate offers stability but only provides a single-disbursement, lump sum of cash at closing. The adjustable-rate mortgage (ARM) is the most popular choice, offering flexible payouts like a line of credit or fixed monthly advances. Consult a reverse mortgage planner to find the best option for you.

Myth #15: You won’t ever be able to sell and move.

You can sell your home and move at any time. When you sell, you’ll need to repay the reverse mortgage loan balance, but you can use the proceeds from the sale to do so.

Let’s Start a Conversation!

If you’d like to learn more about reverse mortgage loans and how one may help with your unique needs, those of a loved one or someone you advise, connect with Fairway today to learn more.

*This advertisement does not constitute tax or financial advice. Please consult a tax professional or financial advisor regarding your specific situation.

**There are some circumstances that will cause the loan to mature and the balance to become due and payable. Borrower is still responsible for paying property taxes and insurance and maintaining the home. Credit subject to age, property and some limited debt qualifications. Program rates, fees, terms and conditions are not available in all states and subject to change.

***The required down payment on your new home is determined on a number of factors, including your age (or eligible non-borrowing spouse’s age, if applicable); current interest rates; and the lesser of the home’s appraised value or purchase price.