Unlocking Financial Flexibility: Harnessing the Power of the HECM Line of Credit

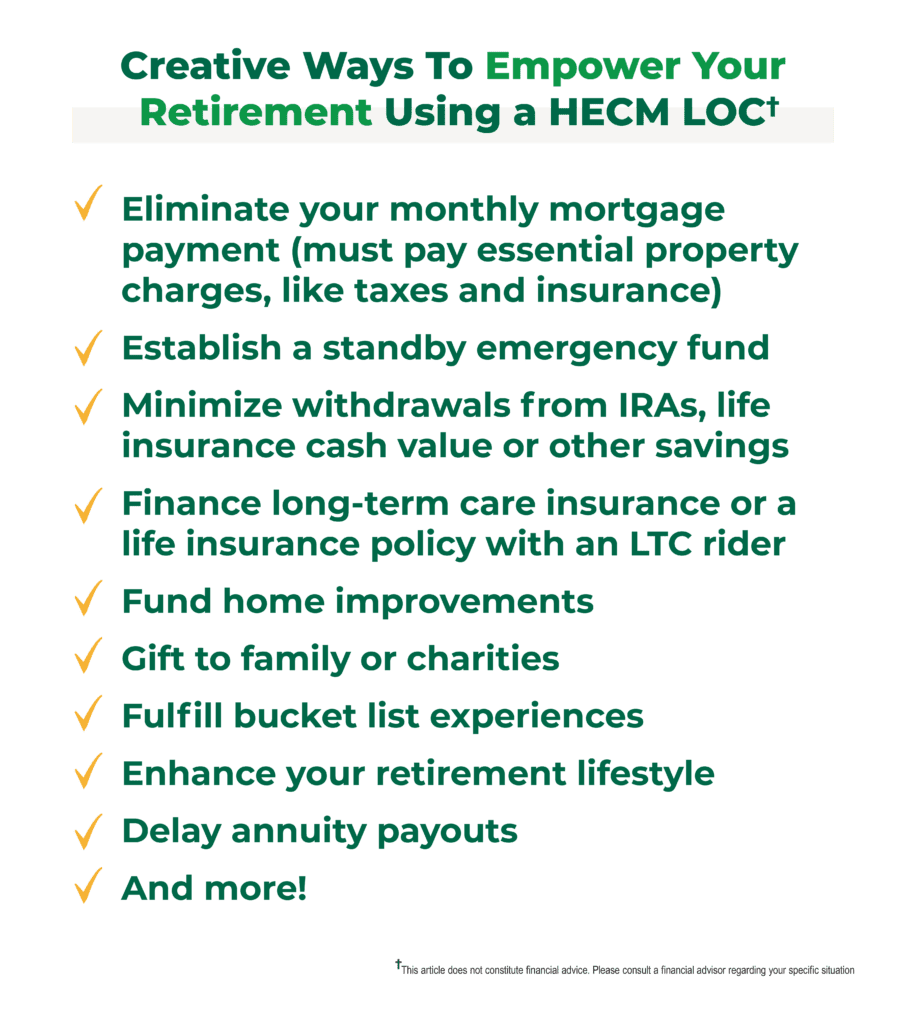

Retirement is often seen as a period of fulfillment. Yet, many retirees encounter challenges such as ongoing mortgage payments, inadequate funds for unforeseen expenses like in-home care or a retirement lifestyle that doesn’t align with their lifelong aspirations.

Enter the HECM line of credit (HECM LOC), a Home Equity Conversion Mortgage (HECM, reverse mortgage) loan feature designed to provide older homeowners with a versatile contingency fund. This Federal Housing Administration (FHA)-insured loan option allows you to bolster your monthly cash flow, address unforeseen expenses and elevate your lifestyle in retirement.

While traditional Home Equity Lines of Credit (HELOCs) are available, the HECM LOC stands out by catering to older Americans’ specific needs and cash-flow concerns.

In this article, we delve into what a HECM entails, weigh the pros and cons of the HECM line of credit and explore how today’s seniors are leveraging it to enrich their retirement years.

This article covers:

- What Is a HECM?

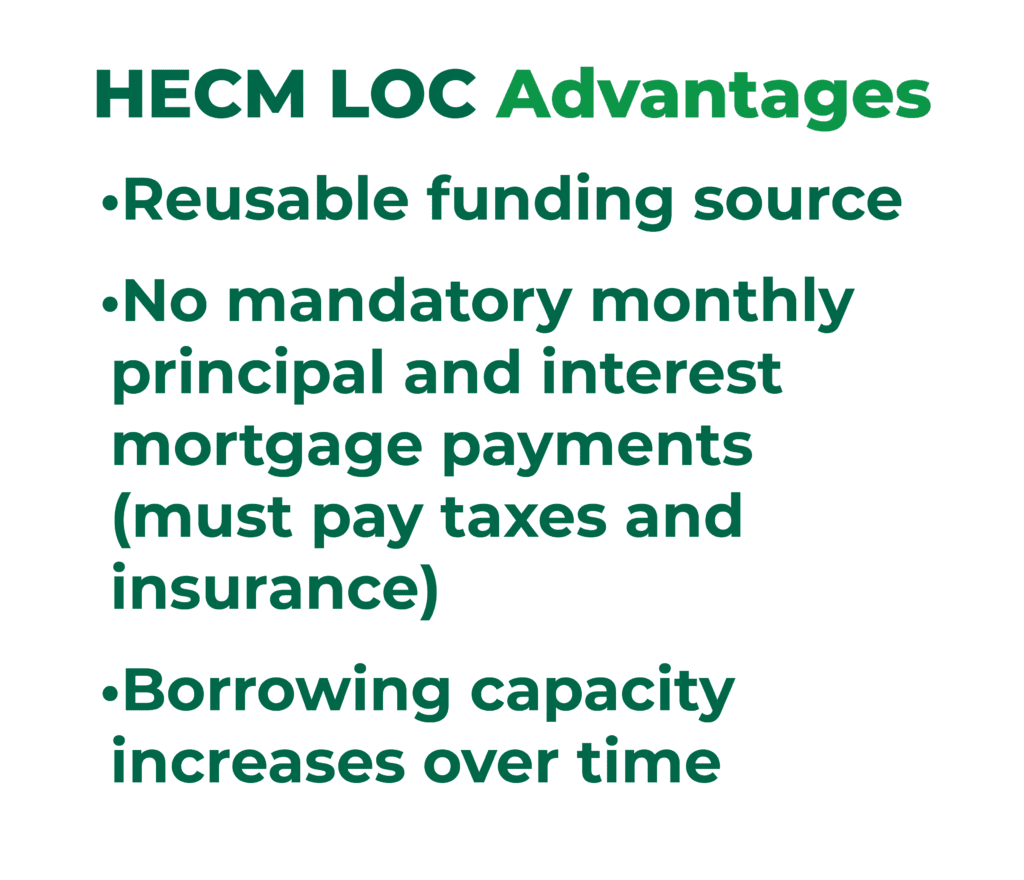

- HECM LOC Advantages

- Reusable funding source

- No mandatory monthly principal and interest mortgage payments (Borrower must still pay taxes and insurance and maintain the home)

- Line of credit cannot be canceled, frozen or reduced due to market conditions

- Line of credit draw period extends to the youngest borrower’s 150th birthday

- Borrowing capacity increases over time

- Generally easier for older adults to qualify (compared to traditional mortgages)

- Borrower/heirs aren’t liable for repaying a loan balance exceeding the home value

- Fees and interest don’t accrue on the unused portion of the credit line

- Can be combined with fixed monthly installment payouts

- HECM LOC Disadvantages

What Is a HECM?

A Home Equity Conversion Mortgage enables homeowners 62 and over to access a portion of their home equity through a lump sum, line of credit or monthly installments. Typically, repayment isn’t required until the last borrower sells the home, moves out or passes away. While no monthly mortgage payments are necessary, the borrower must reside in the home, maintain it and cover essential property expenses like taxes and insurance.

HECM LOC Advantages

Reusable Funding Source

Similar to a credit card, the HECM LOC allows borrowers the flexibility to borrow available funds, repay them and borrow again as needed. Funds the borrower requests from the accessible line of credit will be wired into the borrower’s bank account within five business days.

No Mandatory Monthly Principal and Interest Mortgage Payments

Unlike a traditional HELOC, a HECM LOC doesn’t require monthly mortgage payments. While repayment of the HECM loan balance can be deferred until the last remaining borrower passes away or moves out, the borrower must maintain the home and pay the essential property charges, like taxes and insurance.

If you currently have a traditional mortgage, you can use loan proceeds at closing to refinance (pay off) that mortgage. In other words, you’d be swapping your monthly-payment-required mortgage for a new mortgage in which monthly principal and interest mortgage payments are optional.

Line of Credit Cannot Be Canceled, Frozen or Reduced Due to Market Conditions

Amidst the 2008 financial crisis and the 2020 global pandemic, a notable concern emerged as some HELOC lenders opted to terminate, freeze or reduce the remaining available credit lines for certain borrowers.

Unlike HELOCs, with a HECM LOC, the available line of credit remains guaranteed and accessible, irrespective of fluctuations in home values or market conditions. As long as the borrower adheres to the agreed-upon loan terms established at closing, access to the line of credit is assured.

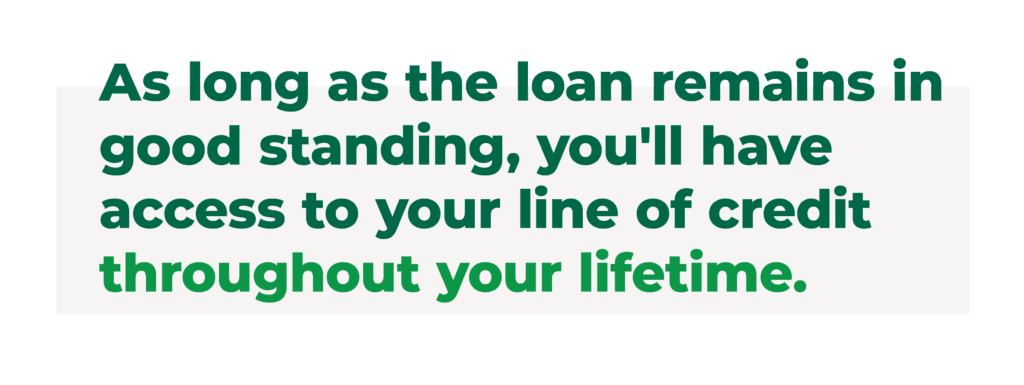

Line of Credit Draw Period Extends to the Youngest Borrower’s 150th Birthday

As long as the loan remains in good standing, you’ll have access to your line of credit throughout your lifetime. This is a significant advantage over traditional HELOCs, which often have shorter draw periods of five to ten years. Once the draw period ends in a HELOC, borrowers can no longer access the line of credit, and the repayment period begins, requiring repayment of both the principal and interest on the loan.

Borrowing Capacity Increases Over Time

The available borrowing capacity increases progressively as the unused portion of the HECM line of credit grows at the same compounding rate as the loan balance, resulting in enhanced borrowing potential over the years. Therefore, initiating the HECM line of credit sooner rather than later can prove advantageous.

To illustrate, consider the following example based on a monthly interest rate of 6.75% and no withdrawals made:

Initial Line of Credit: $200,000

In 5 years: $287,070

In 10 years: $412,056

In 20 years: $848,911

Generally Easier for Older Adults To Qualify (Compared To Traditional Mortgages)

Qualifying for a HECM LOC usually entails less rigorous criteria than HELOCs or traditional mortgages.

For example, there’s no minimum credit score requirement. Instead, the lender evaluates the applicant’s credit history, property charge history and monthly residual income to assess loan approval. The emphasis is on ensuring that the borrower has the financial capability to fulfill the loan terms, including continuous payment of property-related taxes and insurance.

Additionally, for borrowers with a blemished credit history, there may be an option to set aside funds to cover ongoing essential property charges such as taxes and insurance.

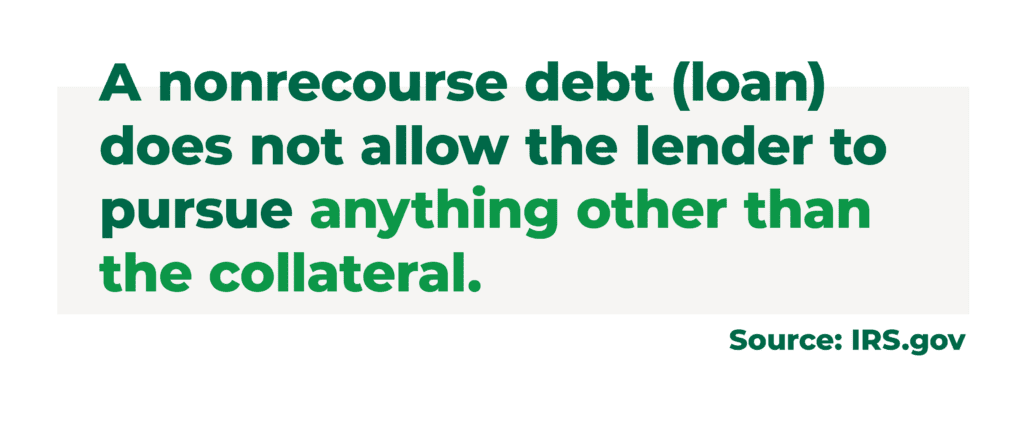

Borrower/Heirs Aren’t Liable for Repaying a Loan Balance Exceeding the Home Value

A HECM is a non-recourse loan, meaning that if the loan balance surpasses the home’s value when due, the home sale will cover the loan, and neither the borrower nor their heirs will be obligated to pay the shortfall.* If the home’s value exceeds the loan balance at maturity, the borrower or heirs retain any remaining proceeds after settling the loan.

Fees and Interest Don’t Accrue on Unused Portion of the Credit Line

The borrower only accrues charges on what they borrow. Notably, there’s no obligation for the borrower to utilize the line of credit unless they opt to do so.

Can Be Combined With Fixed Monthly Installment Payouts

Instead of solely opting for a line of credit, you can combine the line of credit with regular monthly payouts for the duration of your residency in the home (or for a fixed period of months). These are just some of the payout options available to HECM borrowers.

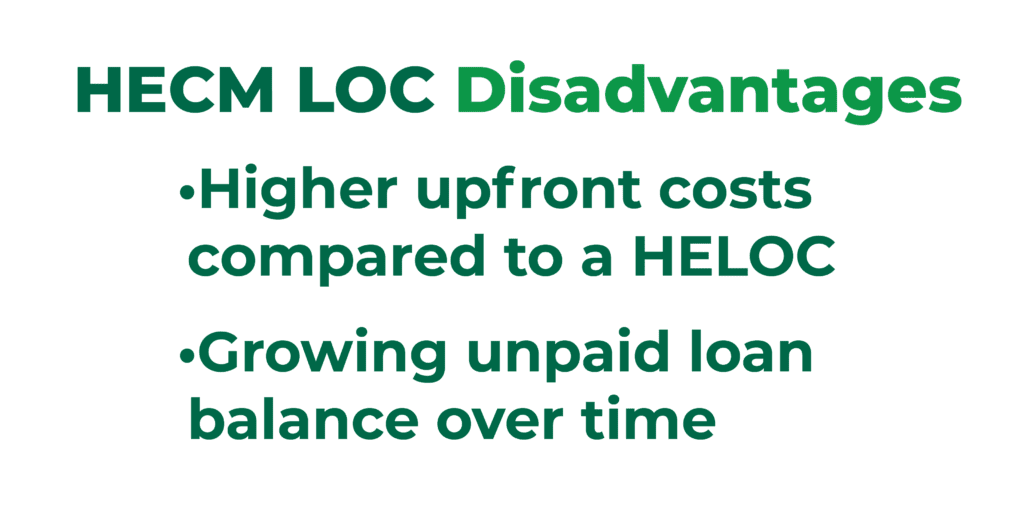

HECM LOC Disadvantages

Higher Upfront Costs Compared to a HELOC

While most of the expenses associated with a HECM LOC can be rolled into the loan, HELOCs typically involve lower upfront costs. However, the benefits of the HECM LOC may outweigh these initial expenses. For a detailed breakdown of HECM loan costs, click HERE.

Growing Unpaid Loan Balance Over Time

The outstanding balance on a reverse mortgage loan increases gradually due to accrued interest and fees added to the unpaid balance. Nonetheless, you can pay down the loan balance at your discretion.

Potential Impact on Eligibility for Needs-Based Programs

While having funds available in a line of credit generally doesn’t affect eligibility for needs-based government programs like Medicaid, depositing large sums of money into a bank account can. It’s advisable to seek guidance from a trusted financial advisor or benefits administrator regarding matters related to government benefits.

Only Available as a Variable-Rate Loan

The HECM LOC is solely offered as an adjustable-rate loan. The interest rate is tied to an index, resulting in monthly or annual adjustments. Fixed-rate HECMs are available for a single lump sum payout of loan proceeds at closing.

Let’s Start a Conversation!

A HECM line of credit offers many benefits and could be a cornerstone of your retirement strategy, providing enhanced financial flexibility for the future. As a reputable FHA-approved lender, Fairway Independent Mortgage Corporation is committed to providing comprehensive insights into the advantages and drawbacks of utilizing your home equity through a HECM LOC.

Connect with us today to explore the potential of your home equity.

*There are some circumstances that will cause the loan to mature and the balance to become due and payable. Borrower is still responsible for paying property taxes and insurance and maintaining the home. Credit subject to age, property and some limited debt qualifications. Program rates, fees, terms and conditions are not available in all states and subject to change.