The Reverse Mortgage Loan Line Of Credit

The Swiss Army Knife Of Financial Planning

Of the challenges that financial planners face in shepherding clients through retirement, cash flow and risk management are among the most common. The reverse mortgage loan line of credit offers immediate solutions for both of these issues and more. With a unique value growth feature, it offers the opportunity for retirement funds to last a lifetime, even with unexpected living expenses and market volatility. Here’s why the reverse mortgage loan line of credit is a powerful tool for a variety of clients and financial situations.

What Is the Reverse Mortgage Loan Line of Credit?

It’s an option for receiving loan proceeds from a reverse mortgage loan. The same rules and protections apply just as if a client received a reverse mortgage loan with a lump sum payment. Most notably, it eliminates obligatory monthly mortgage payments (the borrower must still pay taxes, insurance, and maintain the home), offers potential tax advantages*, and the borrower will never be required to pay more than the home is worth.**

What makes it different is that the borrower can use as much cash as they want from loan closing through the first twelve months (up to the max limit set by HUD), and the remaining credit can be accessed as needed. But this in and of itself is not what makes the reverse mortgage loan line of credit so useful for so many different people.

The Line of Credit Grows Over Time

As with any loan balance that is not repaid, it accrues interest over time. But a reverse mortgage loan line of credit grows at the selected rate, plus a fixed lender’s margin set in the contract, and a fixed mortgage insurance premium of .5%. This combination of three factors is “the effective rate.”

What’s special is that the effective rate applies to not only the loan balance, but also the overall principal limit. This principle limit is the sum of the loan balance, the remaining line of credit, and any set-asides. In other words, with the reverse mortgage line of credit, the unused portion of the line of credit grows at the same compounding rate as the loan balance. That line of credit is open-ended, allowing your clients to borrow from the line of credit, pay it back, then borrow or let it grow again.

With The Reverse Mortgage Line Of Credit, The Unused Portion Of The Line Of Credit Grows At The Same Compounding Rate As The Loan Balance.

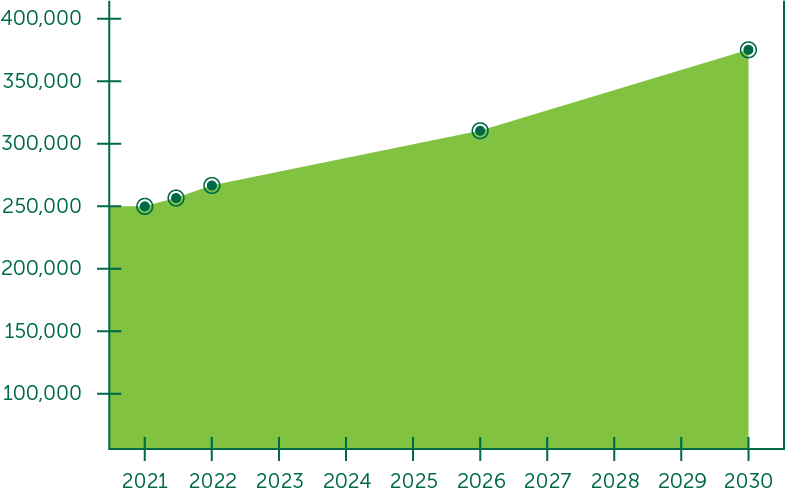

That offers the ability for your clients to have access to more and more cash from their reverse mortgage loan as they move through retirement. Here’s a sample scenario of what a reverse mortgage loan line of credit can offer.

Index + Margin = 4.00%

Mortgage Insurance Premium = .5

Available Credit to Begin = $250,000

Credit After 6 Months = $255,625

Credit After 12 Months = $261,250

Credit After 5 Years = $306,250

Credit After 10 Years = $362,500

See what you can qualify for by using our reverse mortgage calculator.

Financial Security & Flexibility

Unlike traditional lines of credit through a bank, a reverse mortgage loan line of credit is federally insured and can never be frozen. Additionally, when it comes time for your client to leave the home and settle the loan, they or their heirs would never have to pay more than the market value of the home**—that same insurance would take care of potential overages.

One of the most appealing aspects of the reverse mortgage line of credit is avoiding the sequence of returns risk. As it happens so often to retirees who depend on investments to maintain their quality of life, market volatility can cause immense levels of stress. But with a reverse mortgage loan line of credit, they can draw from their investments when the market is up, and draw from their line of credit when the market is down. This strategy could be used for tax mitigation purposes as well.*

Get to Know This Product Category

The reverse mortgage loan line of credit could make retirement more enjoyable and financially secure for many people. Reach out to Fairway for more in-depth information and hands-on explanations of what this product category could offer to your clients.

Tools for Financial Planners

Did you know that we have a proprietary tool called EquityTrax that maps home equity outlook throughout retirement?

Learn More

If you’re interested in learning more, reach out to a Fairway reverse mortgage specialist today. Fairway offers the Home Equity Line of Credit (HECM), Jumbo Reverse Mortgage, and Reverse Mortgage for Purchase Loan (H4P).

*This advertisement does not constitute tax and/or financial advice from Fairway

** There are some circumstances that will cause the loan to mature and the balance to become due and payable. Borrower is still responsible for paying property taxes and insurance and maintaining the home. Credit subject to age, property and some limited debt qualifications. Program rates, fees, terms and conditions are not available in all states and subject to change.