How a Reverse Mortgage Loan Can Enhance a Sound Retirement Strategy

These days, people are living longer, which, of course, is a good thing. But it also means retirees’ savings must stretch further to last throughout retirement. Throw in the recent surge in inflation and the unfortunate reality that many retirees are not financially prepared for retirement, and we have the makings of a retirement crisis ahead.

On the bright side for older-adult homeowners, housing wealth has been on the rise. According the National Reverse Mortgage Lenders Association (NRMLA), U.S. homeowners aged 62+ saw their home equity soar to a record $10 trillion in 2021. It can be prudent for homeowners and their advisors to discuss ways to incorporate housing wealth into retirement planning decisions.

What Is a Reverse Mortgage Loan?

A Home Equity Conversion Mortgage (HECM, commonly called a reverse mortgage) is a home loan that allows homeowners aged 62 and older to convert a percentage of their home equity into cash or a growing line of credit. The borrower can defer repayment of the loan balance so long as they live in the home and pay the property-related taxes, insurance, and upkeep expenses.

Borrowers have several options for how they can take the loan proceeds:

- A one-time lump sum disbursement

- Fixed monthly advances (for a set number of months or for the life of the loan)

- A line of credit to use as needed

- A combination of the above methods

Note: This article only refers to HECM reverse mortgages, the most popular reverse mortgage product on the market and the only one insured by the Federal Housing Administration (FHA).

Why Might Someone Get a Reverse Mortgage?

Urgent financial need.

Prior to the housing crisis in 2008, reverse mortgages were primarily used by borrowers as a loan of last resort. The borrowers tended to be further along into retirement, house rich, and cash poor. They typically had an immediate need for the cash. For example, the borrower may begin using the loan proceeds right away to pay for their in-home care. They may also want to avoid the burden of fixed monthly mortgage payments in retirement by refinancing into a reverse mortgage (they would still be responsible for paying the property-related charges). But now, reverse mortgages are no longer a loan of last resort and should be treated as a financial vehicle to maximize near all-time highs in home equity.

Lifestyle enhancement.

Some borrowers do not necessarily need to access the equity in their homes, but they take out a reverse mortgage to extend the reach of their budget in order to enhance their lifestyle. This may include things like making their home more comfortable and safe to live in (e.g., upgrading their kitchen and installing a walk-in bathtub). Reverse mortgages also appeal to those who want to live a greater legacy with family — the increased cash flow in retirement can make life a little easier for them.

Financial planning.

Now, more than ever, reverse mortgage borrowers are strategically using their home equity at the earliest age possible to potentially increase their odds of a better retirement outcome. They still may be working, and many are very well off financially, but they realize the potential strategic planning advantages of using home equity, and consequently reverse mortgages, as part of their retirement plan.

The Advantages of The HECM Line of Credit

The most popular option to access HECM reverse mortgage funds, especially for a “planning” borrower, is via the line of credit. Here are the primary advantages of the HECM line of credit.

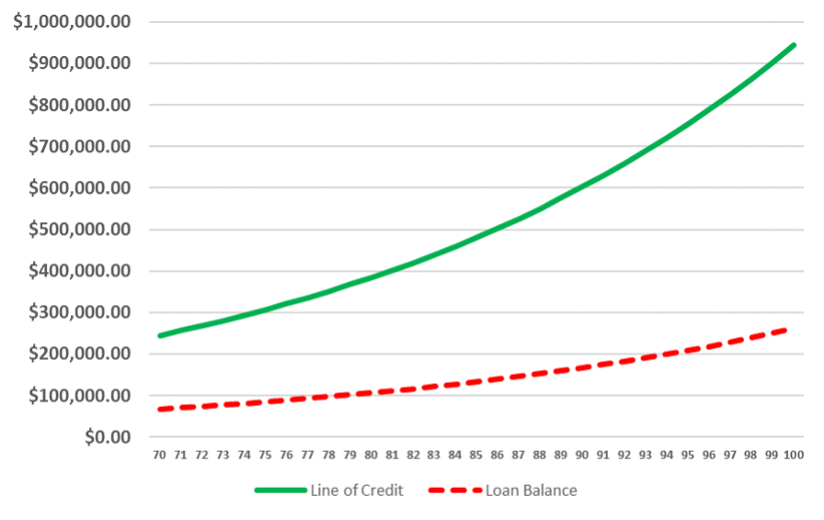

The unused portion of the HECM credit line grows over time.

The unused portion of the credit line grows at the same compounding accrual rate (the interest rate plus 0.50%) as the loan balance, independent of swings in the value of the home. In other words, the borrower will have greater capacity to borrow more funds in the future, if needed. For this reason, it can be valuable to establish the HECM line of credit sooner rather than later.

Here’s an example of how an unused line of credit grows over time versus a loan balance in which no voluntary prepayments are made.

- Home value: $600,000

- Age: 70

- Expected interest rate: 4.00%

- Initial principal limit: $313,200

- Initial loan balance: $68,000 including payoffs and closing costs

- Initial line of credit: $245,200

This information is provided as a guideline and does not reflect the final outcome for any particular homebuyer or property. The actual reverse mortgage available funds are based on current interest rates, current charges associated with loan, borrower date of birth (or non-borrowing spouse, if applicable), the property sales price and standard closing cost. Interest rates and loan fees are subject to change without notice. Following the closing of the home purchase, no further principal or interest payments will be required as long as one borrower occupies the home as their primary residence and adheres to all HUD guidelines of loan. Borrower must remain current on property taxes, homeowner’s insurance (and homeowner association dues, if applicable), and home must be maintained.

The borrower is not charged interest on the funds left in the line of credit.

You can simply leave the unused funds in the line until they’re needed, without accruing interest owed.

The HECM line of credit cannot be frozen, reduced, or canceled.

In retirement, it can be wonderful peace of mind to know the available funds will be there if and when you need them. As long as you meet the loans terms — which include residing in the home and paying the property-related charges, like taxes and insurance — then no one, including the lender, can cancel your line of credit, even if your financial picture changes or your home decreases in value.

Draws from the HECM line of credit are not taxed as income*.

Disbursements from a reverse mortgage are not taxed as income, which can help you to keep your adjusted gross income low.*

How Are Reverse Mortgages Being Used for Financial Planning?

Before we dive in, let’s level-set. Fairway Independent Mortgage Corporation is a lender — we are not in the business of giving tax, legal, or investment advice; thus, the content from this article should not be perceived as such. We encourage you to speak with a financial planning professional to explore the pros or cons of strategically using home equity, and we welcome the opportunity to be a participant in those conversations.

Using a reverse mortgage to help protect investments*.

During one’s working years, investment tends to be a means to accumulate money for retirement. During retirement, one’s investment strategy usually switches to being more focused on minimizing risks and protecting investments, so the funds last as long as possible. The HECM line of credit can be used to help protect investments — the effectiveness of such use cases has been confirmed in multiple studies conducted by various academics with no ties to the mortgage industry.

According to research† conducted by scholar John Salter, Ph.D., CFP®, AIFA®, using a reverse mortgage line of credit as standby portfolio protection can dramatically reduce what he calls “volatility drain,” which is caused by selling investments when the market is down. A HECM line of credit allows a homeowner to draw needed cash flow, usually tax free, from their home equity, during market downturns. This has been shown mathematically to extend a retiree’s traditional investments.*

The second part of this strategy is that many investors will take their gains during a bull market and pay down their reverse mortgage loan balance. This technique allows the borrower to boost their line of credit, which they can choose to let grow again, for any future needs.

Using a reverse mortgage to minimize taxes in retirement.*

As previously mentioned, the reverse mortgage loan proceeds are usually tax free. An example of a way a borrower may be able to use a reverse mortgage to minimize taxes in retirement is to use the loan proceeds to pay the upfront tax liabilities when they are moving money from a traditional pre-tax retirement account into a post-tax Roth account. This can create cash-flow flexibility and potentially lead to a bigger Roth account and greater net worth.*

Using a reverse mortgage as a protective hedge for home values.

We discussed how the unused portion of the HECM line of credit is guaranteed to grow over time independent of home values. Now, let’s bring to light this complementary benefit: The HECM borrower (or their heirs) can never owe more than the home is worth at the time of loan maturity.** The loan most commonly reaches maturity and is due and payable when the last remaining borrower permanently moves out of the home or passes away.

The loan is then typically satisfied by the sale of the home. Since a HECM reverse mortgage is a non-recourse loan insured by the FHA, even if the loan balance exceeds what the is home worth, the sale of the home will satisfy the loan and neither the borrower nor their heirs will not be responsible for paying the difference.

Using a reverse mortgage to offset financial shocks.

Any financial shock, like a loss of income due to a loss of a spouse, can make meeting financial goals in retirement a more difficult task. A reverse mortgage line of credit can serve as a source of reserve to cover unexpected spending needs.

Get to Know Today’s HECM Reverse Mortgages — and What They Can Do for You and Your Retirement

A reverse mortgage can be a great option to help you make the most of your retirement cash-flow strategy. We know that the decision of whether to use home equity in retirement is often a family decision, and we encourage open dialog among you, your family, your financial advisor, and our team. Let’s start a conversation — connect with a Fairway Retirement Mortgage Specialist today!

*This advertisement does not constitute tax or financial advice. Please consult a tax advisor or financial advisor regarding your specific situation.

**There are some circumstances that will cause the loan to mature and the balance to become due and payable. Borrower is still responsible for paying property taxes and insurance and maintaining the home. Credit subject to age, property and some limited debt qualifications. Program rates, fees, terms and conditions are not available in all states and subject to change

†Source: Journal of Financial Planning: August 2012 https://www.financialplanningassociation.org/article/journal/AUG12-standby-reverse-mortgages-risk-management-tool-retirement-distributions

Copyright©2022 Fairway Independent Mortgage Corporation (“Fairway”) NMLS#2289. 4750 S. Biltmore Lane, Madison, WI 53718, 1-866-912-4800. All rights reserved. Fairway is not affiliated with any government agencies. These materials are not from HUD or FHA and were not approved by HUD or a government agency. Reverse mortgage borrowers are required to obtain an eligibility certificate by receiving counseling sessions with a HUD-approved agency. The youngest borrower must be at least 62 years old. Monthly reverse mortgage advances may affect eligibility for some other programs. This is not an offer to enter into an agreement. Not all customers will qualify. Information, rates and programs are subject to change without notice. All products are subject to credit and property approval. Other restrictions and limitations may apply. Equal Housing Opportunity.