Mastering the Market Shift: How Home Equity Conversion Mortgage for Purchase (H4P) Loans Turn Challenges Into Opportunities for Loan Officers and Realtors

In a recent MBA Newslink article, John McMullen, Senior Policy Specialist at the Mortgage Bankers Association, revealed the transformative power of the H4P (Home Equity Conversion Mortgage for Purchase) loan for homebuyers 62 and older. This article delves into those insights, showcasing how this innovative loan enables seniors to achieve their ideal retirement homes, improve cash flow and protect savings—while offering a strategic advantage for housing professionals navigating today’s market.

Since 2022, elevated mortgage rates have put the brakes on refinance opportunities for many mortgage professionals. Coupled with scarce inventory and shrinking housing affordability, these factors dampened purchase activity.

However, there’s a silver lining—the Home Equity Conversion Mortgage for Purchase (H4P) loan program. This little-known yet powerful tool helps Americans 62 and older secure their dream retirement homes, enhance cash flow and preserve their savings, transforming market challenges into lucrative opportunities for housing-sector professionals.

This article covers:

- What Is an H4P Loan

- Why You Should Add H4P to Your Offerings

- Why H4P Makes Sense Now

- The Fairway Advantage

What Is an H4P Loan?

The H4P loan is regulated by the Department of Housing and Urban Development (HUD) and insured by the Federal Housing Administration (FHA). Highlighted in an MBA Newslink article by John McMullen, AMP, as a smart strategic move for Independent Mortgage Banks (IMBs), H4P loans offer a unique route for homebuyers 62 and older, diverging from traditional mortgages.

Often dubbed as a reverse mortgage for purchase, the H4P loan empowers seniors to buy a new primary residence with enhanced repayment flexibility.

Here’s how it works:

Initial Contribution

Borrowers usually put down just 50%-70%* of the home’s purchase price, often using proceeds from selling their current home or personal savings. (Curious about how much cash your client will need to close? Use our digital calculator for a quick estimate.)

Remaining Balance

The lender finances the rest. No monthly principal and interest mortgage payments are required—the borrowers only need to cover essential property charges like taxes and insurance. Over time, the unpaid loan balance accrues compounding interest (negative amortization).

Repayment

Generally, the loan is due when the last surviving borrower leaves or passes away and is typically paid off through the home’s sale. Heirs can keep the home by refinancing for the lesser of the loan balance or 95% of the home’s value.

With mortgage insurance premiums (MIPs), H4P loans ensure borrowers and their heirs never owe more than the home’s value when repayment is due and the home is sold. The FHA’s Mutual Mortgage Insurance Fund covers any shortfall, protecting against liabilities beyond the home’s worth.**

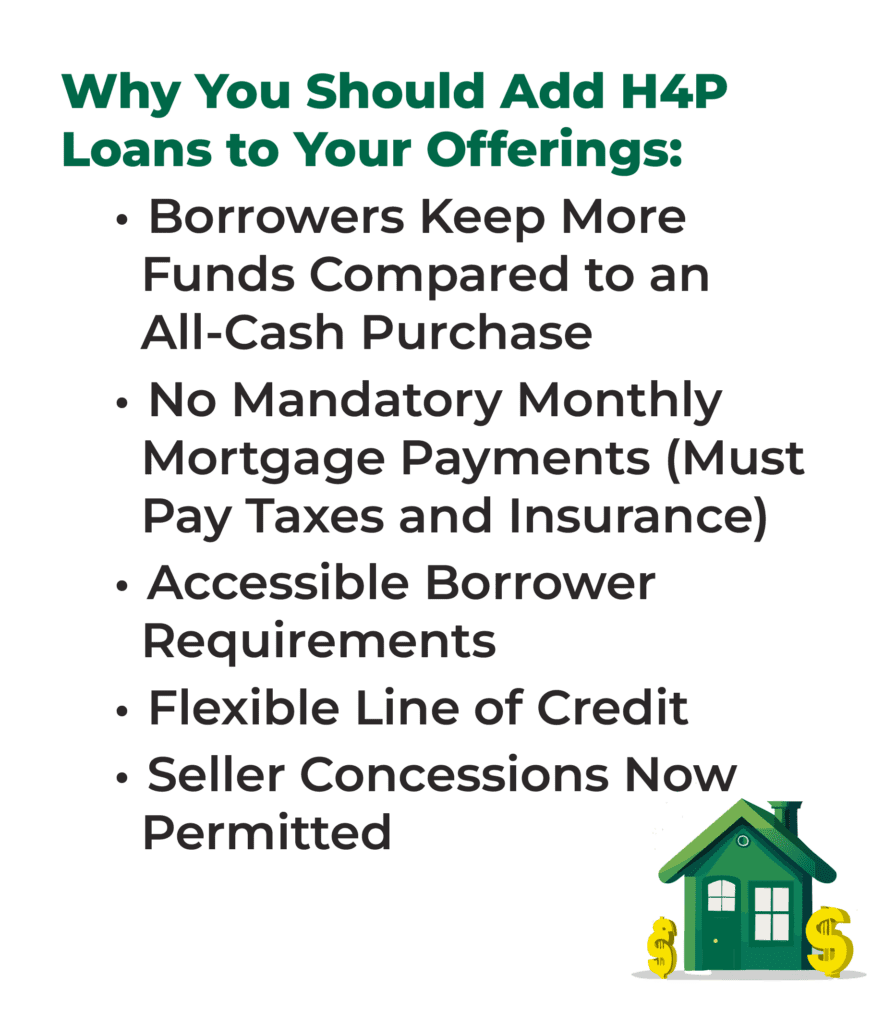

Why You Should Add H4P to Your Offerings

H4P loans offer myriad benefits for senior homebuyers, enhancing your value proposition. Here are key reasons your older clients will be eager to explore this option.

Borrowers Keep More Funds Compared to an All-Cash Purchase

Buying a home with cash eliminates mortgage payments but ties up significant funds in a non-liquid asset, reducing financial flexibility. With an H4P, clients can finance part of the purchase, avoid monthly principal and interest mortgage payments (must pay essential property charges, like taxes and insurance) and keep more funds available for other uses. This preserves assets and maintains cash flow, helping manage retirement risks like inflation and unexpected expenses.

No Mandatory Monthly Mortgage Payments (Must Pay Taxes and Insurance)

Traditional mortgages require less upfront cash but come with decades of monthly principal and interest payments, straining retirement cash flow. For example, a 65-year-old buying a $600,000 home with a traditional 30-year mortgage ($120,000 down, $480,000 financed) at 7.15% interest would face monthly principal and interest payments of $3,242 and total loan costs (excluding closing costs) of $1,167,103.

In contrast, an H4P could allow that homebuyer to finance the $600,000 home with an upfront investment of $411,000 and no monthly mortgage payments (must pay essential property charges, like taxes and insurance), streamlining cash flow management over time while enjoying full ownership of their new home.

Accessible Borrower Requirements

Due to strict qualification criteria, traditional mortgages can be tough for seniors with low income or credit challenges. According to Mayer and Moulton’s research, in 2018 alone, over 210,000 mortgage applications from those 62 and older—34% of their total—were rejected or withdrawn because of high debt-to-income ratios.

By contrast, H4P loans have less restrictive qualification requirements. They focus on a borrower’s ability to cover ongoing property charges rather than ongoing property charges and monthly principal and interest mortgage payments, making them a more accessible option. This gives loan officers and real estate professionals a valuable opportunity to successfully close deals that might otherwise fall through the cracks.

Flexible Line of Credit

With an adjustable-rate H4P loan, your clients can unlock a dynamic line of credit that only accrues charges on what they actually borrow. They can activate this credit line with an initial monetary investment above the minimum required. The best part? The unused portion grows at the same compounding rate as the loan balance, boosting borrowing capacity over time. Plus, it’s secure, as the H4P line of credit can’t be canceled, frozen or capped due to market conditions.

Seller Concessions Permitted

The FHA has updated the H4P loan program to better align with other FHA mortgages. Property sellers, real estate agents, builders or developers can now contribute up to 6% of the sales price—something that was previously off-limits.

Why H4P Makes Sense Now

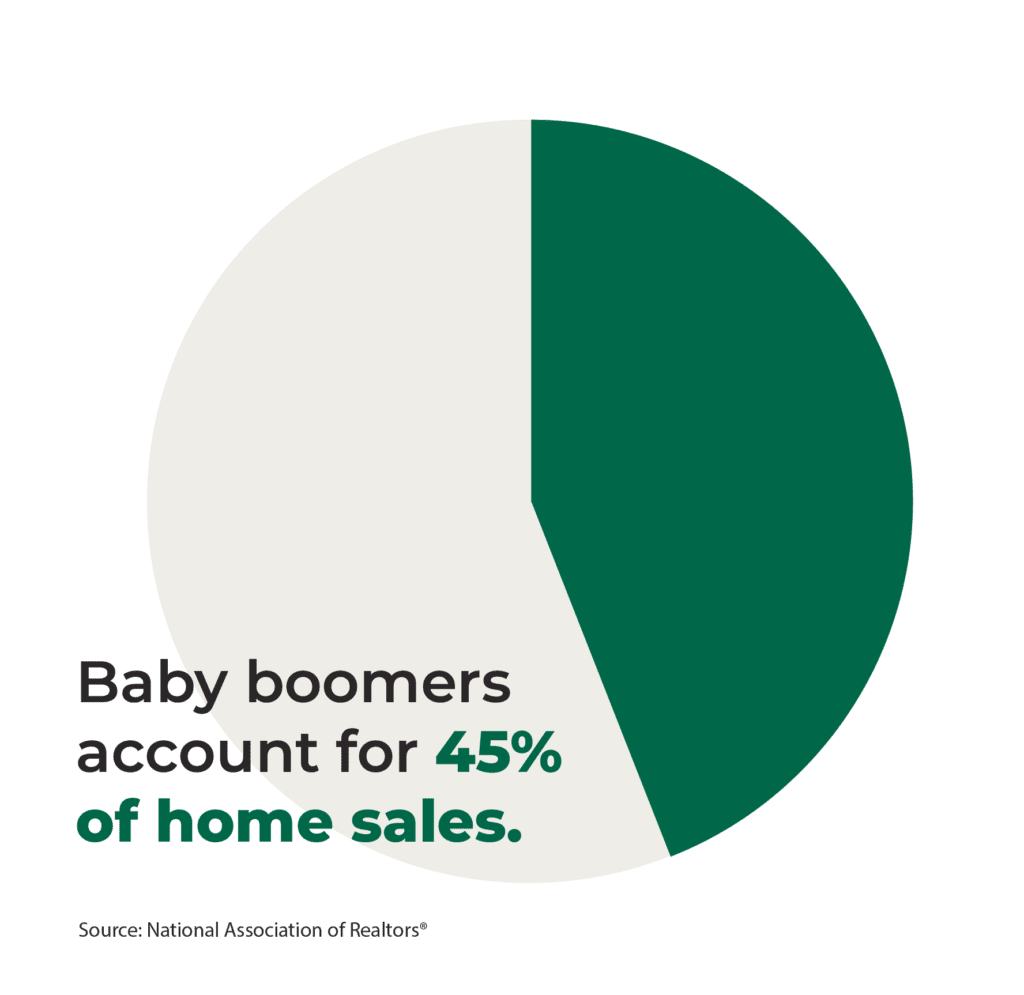

Today’s market challenges affect everyone in the housing sector—lenders, loan officers, buyers and real estate professionals. Older Americans, a vital part of the economic landscape, are eager homebuyers with compelling reasons to purchase a new primary residence. Whether it’s to be closer to family, enjoy single-story living or adopt a low-maintenance lifestyle, the desire is strong. Yet, many seniors with low-rate mortgages from 2020-2021 now face around 7% rates, making moving costly.

The H4P program offers seniors a clever way to navigate high interest rates, enhance their buying power and secure their dream homes without the burden of monthly mortgage payments (must pay essential property charges, like taxes and insurance). This makes the transition into retirement smoother and more affordable. With baby boomers accounting for 45% of home sales, tailoring loan products to meet their specific needs can unlock substantial opportunities in this expanding market.

As John McMullen noted, “With the economic landscape in flux and over 12,000 Americans turning 65 daily in 2024, the market for this [H4P] program is set for significant growth.”

The Fairway Advantage

Fairway Independent Mortgage Corporation (NMLS #2289) stands out as a top-tier full-service mortgage lender renowned for innovative homeownership solutions. Fairway, rated #1 in Mortgage Origination Customer Satisfaction for 2023 by J.D. Power and a leading H4P lender, brings unmatched excellence and expertise to every loan.

Fairway Reverse, a specialized division, empowers older-adult homebuyers and homeowners. With rapid turnaround times and a commitment to strong customer relationships, Fairway Reverse earned the title of best reverse mortgage company for homebuyers from Money.com. As an FHA-approved lender and proud NRMLA member, we offer unparalleled service.

Our in-house referral program allows Fairway’s network of forward loan officers to offer H4P loans effortlessly without needing extensive training or loan processing challenges. This boosts commissions with minimal sales effort while clients receive top-notch service from our dedicated team of reverse mortgage planners.

Fairway is devoted to educating and partnering with real estate professionals who share our vision of helping older Americans achieve their dream retirements. Based in Madison, Wisconsin, Fairway continues to lead the way in mortgage lending excellence.

Let’s Start a Conversation!

Where your clients choose to live in retirement impacts their family life, hobbies, comfort, safety, cash flow, overall happiness and more. Whether you’re assisting with real estate or financing, the H4P loan presents a golden opportunity to boost home sales and increase margins while offering older clients a powerful new home financing option. Let’s connect to discuss how H4P loans can help grow your business.

*The required down payment on your client’s new home is determined on a number of factors, including their age (or eligible non-borrowing spouse’s age, if applicable); current interest rates; and the lesser of the home’s appraised value or purchase price

**There are some circumstances that will cause the loan to mature and the balance to become due and payable. Borrower is still responsible for paying property taxes and insurance and maintaining the home. Credit subject to age, property and some limited debt qualifications. Program rates, fees, terms and conditions are not available in all states and subject to change.

Copyright©2024 Fairway Independent Mortgage Corporation. NMLS#2289. 4750 S. Biltmore Lane, Madison, WI 53718, 1-866-912-4800. Distribution to general public is prohibited. All rights reserved. Equal Housing Opportunity.